Capital Budgeting: Investment Evaluation Framework

Capital Budgeting evaluates long-term investments using techniques like NPV (Net Present Value), IRR (Internal Rate of Return), and Payback Period to make informed capital allocation decisions.

What Is It?

Capital Budgeting provides rigorous methods for evaluating major investments—new equipment, facilities, acquisitions, or projects. Unlike day-to-day expenses, these decisions commit resources for years and are difficult to reverse.

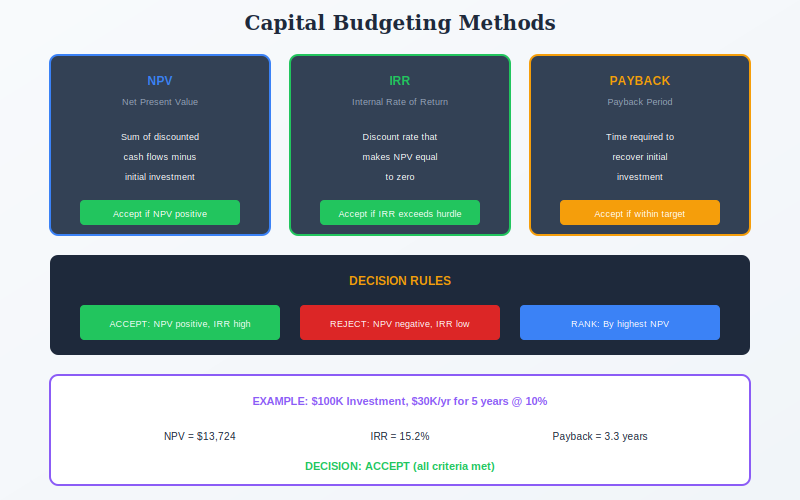

NPV sums discounted future cash flows minus initial investment—positive means value creation. IRR finds the rate where NPV equals zero—compare to your cost of capital. Payback measures time to recover investment—shorter is less risky.

Capital Budgeting connects to Break-Even Analysis for viability assessment and Cash Flow Forecasting for projection inputs.

Quick Reference

Core Features

- NPV (Net Present Value): Absolute value creation measure

- IRR (Internal Rate of Return): Percentage return on investment

- Payback Period: Time to recover initial investment

- Discounted Payback: Payback using present values

- Profitability Index: NPV per dollar invested

- Sensitivity Analysis: Test key assumptions

When to Use

- Major equipment purchases

- Facility expansion or new locations

- Acquisitions and mergers

- New product/service launches

- Technology investments

- Any multi-year capital commitment

When NOT to Use

- Small, routine expenditures

- Emergency or safety-required investments

- Strategic investments defying quantification

- When cash flows are highly unpredictable

- Regulatory compliance requirements

Key Strengths

- Time Value: Properly accounts for money's time value

- Rigorous: Disciplined, quantitative approach

- Comparable: Enables project ranking and selection

- Comprehensive: Multiple methods provide different insights

- Risk-Aware: Sensitivity analysis reveals vulnerabilities

Key Weaknesses

- Highly dependent on cash flow projections

- Discount rate selection is subjective

- May miss strategic/qualitative factors

- Complex for non-financial managers

- IRR can give multiple solutions or misleading results

How It Works

| 1 Primary Input | Initial investment, projected cash flows, discount rate, project life |

|---|---|

| 2 Data You Need | Revenue forecasts, cost estimates, tax impacts, terminal value |

| 3 Primary Output | NPV, IRR, Payback Period, accept/reject recommendation, project ranking |

Comparison with Related Frameworks

Capital Budgeting vs Break-Even Analysis

Break-Even Analysis provides quick viability assessment without time value considerations. Capital Budgeting adds NPV/IRR for rigorous evaluation. Use Break-Even for screening, Capital Budgeting for final investment decisions.

Capital Budgeting vs Cash Flow Forecasting

Cash Flow Forecasting provides the projected cash flows that Capital Budgeting analyzes. Cash Flow Forecasting is the input; Capital Budgeting is the analysis. You need both for sound investment decisions.