Activity-Based Costing: Accurate Cost Allocation

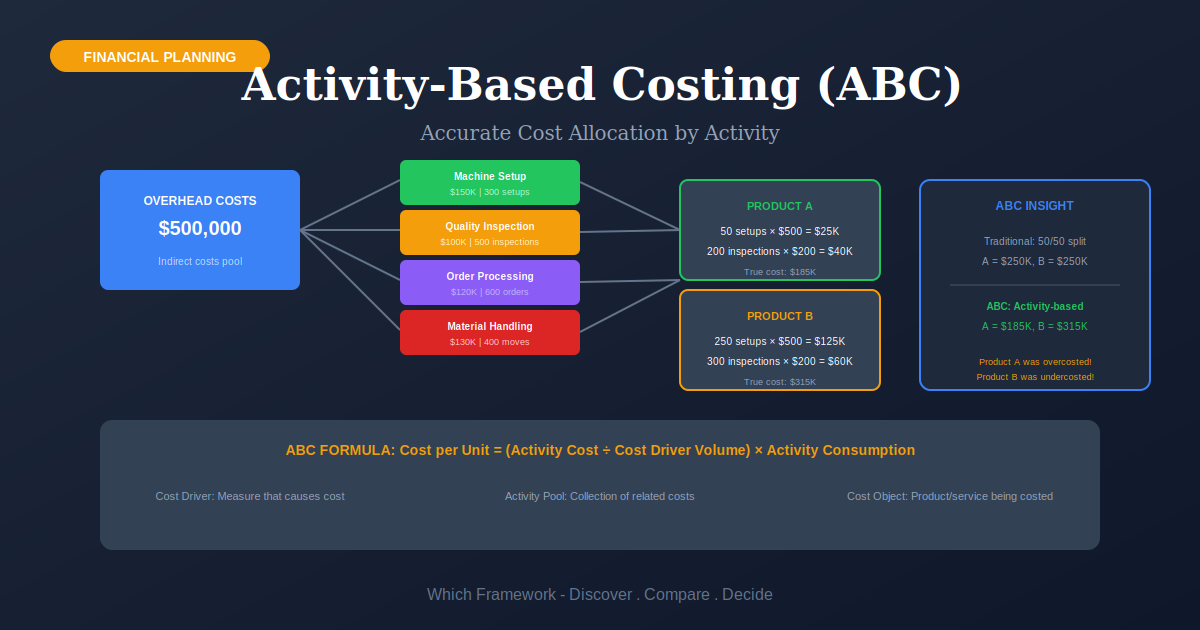

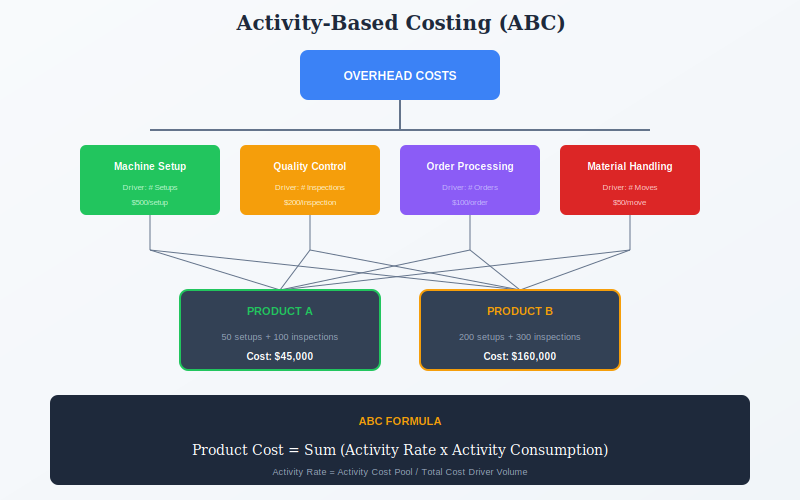

Activity-Based Costing (ABC) allocates overhead costs to products based on the activities they consume, providing more accurate cost information than traditional volume-based allocation.

What Is It?

Traditional costing allocates overhead using simple measures like labor hours or machine hours. ABC recognizes that overhead costs are driven by activities—and different products consume different amounts of these activities.

ABC identifies cost pools (collections of overhead costs) and cost drivers (factors that cause costs). By tracing costs through activities to products, ABC reveals true product profitability—often showing that high-volume simple products subsidize low-volume complex ones.

ABC connects to Zero-Based Budgeting for cost justification and Variance Analysis for performance monitoring.

Quick Reference

Core Features

- Activity Identification: Map all activities that consume resources

- Cost Pools: Group related overhead costs by activity

- Cost Drivers: Identify factors that cause activity costs

- Activity Rates: Calculate cost per unit of driver

- Product Costing: Allocate based on actual activity consumption

- Profitability Analysis: True cost and margin visibility

When to Use

- High overhead costs relative to direct costs

- Diverse product mix with varying complexity

- Strategic pricing decisions

- Product line profitability analysis

- Make vs. buy decisions

- Process improvement initiatives

- Customer profitability analysis

When NOT to Use

- Low overhead environments

- Homogeneous products with similar processes

- When implementation costs exceed benefits

- Organizations lacking data infrastructure

- Stable, well-understood cost structures

Key Strengths

- Accuracy: More precise product and customer costs

- Visibility: Exposes hidden cross-subsidization

- Decision Support: Better pricing and product mix decisions

- Process Insight: Reveals improvement opportunities

- Strategic Alignment: Costs reflect actual resource consumption

Key Weaknesses

- Complex and expensive to implement

- Requires significant data collection

- Can be difficult to maintain over time

- Activity and driver selection requires judgment

- May give false precision if data is poor

How It Works

| 1 Primary Input | Overhead costs, activity analysis, cost driver data |

|---|---|

| 2 Data You Need | Activity costs, driver volumes, product activity consumption |

| 3 Primary Output | Activity rates, accurate product costs, profitability by product/customer |

Comparison with Related Frameworks

Activity-Based Costing vs Zero-Based Budgeting

ZBB decides which costs are worth incurring; ABC tells you what things actually cost. ABC provides data; ZBB makes allocation decisions. Use ABC first to understand costs, then ZBB to optimize spending.

Activity-Based Costing vs Variance Analysis

Variance Analysis compares actual to budgeted costs. ABC provides more accurate cost baselines for variance analysis. Use ABC to set accurate budgets, then Variance Analysis to monitor them.